Reframe Finance #4

Generational wealth, survivorship bias

Hello friends,

Here is your weekly dose of financial wisdom. If you find this newsletter insightful, don’t be selfish: share it with a friend.

Generational Wealth

This week I revisited The Allegory of the Hawk and the Serpent which explores ways to diversify from secular change. A secular market can be defined as driven by forces that cause the asset class to rise or fall over a long period. Here are the key insights:

91% of the price appreciation for a 60% equity 40% bond portfolio over the past 90 years comes from just 22 years between 1984 and 2007.

The successful 100-year portfolio balances assets that profit from secular growth and those that profit from secular decline.

“We cannot solve our problems with the same thinking that created them” — A. Einstein

Prioritize secular non-correlation over excess returns when selecting assets.

True diversification against secular change involves combining offensive assets (stocks, bonds, real estate) and defensive assets (gold, active long volatility, commodity trend following).

For a regular investor, this means finding the right asset allocation between cash, gold, bonds, stocks, and real estate.

Monkeys on Typewriters

“If one puts an infinite number of monkeys in front of typewriters, and lets them clap away, there is a certainty that one of them would come up with an exact version of the Iliad. Now that we have found a hero among monkeys, would you invest your life’s savings on a bet that this monkey would write the Odyssey next?” — N. Taleb, Fooled by Randomness

If someone has performed better than the crowd in the past, there is a presumption of his ability to do better in the future. But this presumption may be very weak because it all depends on two factors:

The profession’s randomness content

The number of monkeys in operation

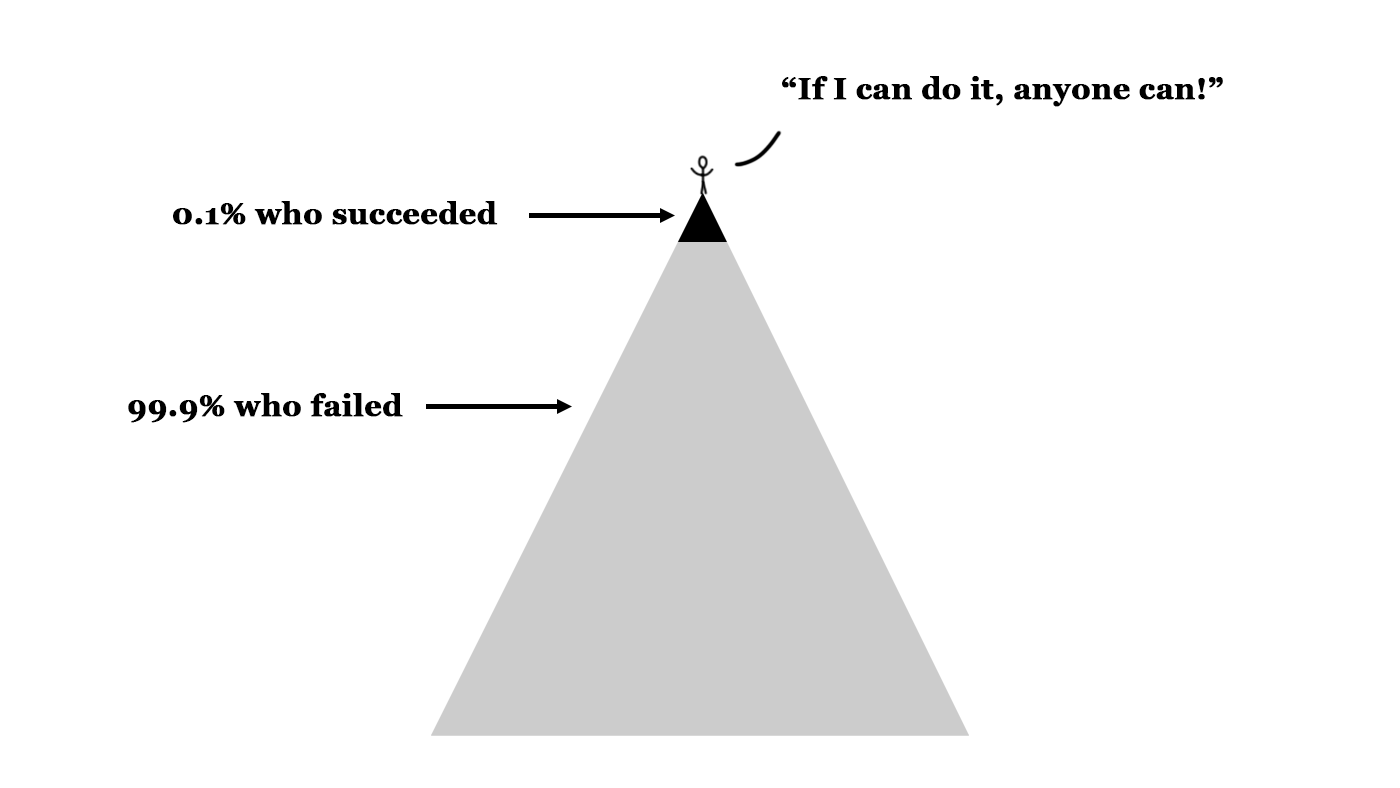

If there are five monkeys in the game, it would be extremely impressive if one of them wrote the Iliad. However, if there are a billion, it would be surprising if none of them got some well-known piece of work, just by luck.

Unfortunately, in real life the other monkeys are uncountable and we only see the winners which gives us a mistaken perception of the odds (i.e. survivorship bias).

“Mild success can be explainable by skills and labor. Wild success is attributable to variance.” — N. Taleb

For example, a population entirely composed of bad managers will produce a small amount of great track records. Therefore, the number of managers with great track records depends far more on the number of people who started in the investment business rather than on their ability to produce profits.

As the saying goes, even a broken clock is right twice a day.

To unconventionality,